Cryptocurrency taxation: the guide (updated 2026)

Summary for busy readers:

- Capital gains on fiat-crypto transactions are taxable

- La Flat rate of 30% applies to these capital gains of (12.8% tax and 17.2% social security contributions).

- Transactions and capital gains must be reported In case of transfers thereupon taxation regime

- Exchange accounts should be Declared yearly

- Finary Automatically calculates your crypto added value

Cryptocurrency taxation: what's changing in 2023

Make the choice of your taxation

As of January 1, 2023, a major change was introduced: Article 79 of the 2022 Finance Act specifies that taxpayers can now opt between two methods of taxation: the fixed rate of 12.8% or the Progressive scale of income tax.

In some particular cases this may be interesting. For example, if an individual is not subject to taxation, they will only be subject to 17.2% social security contributions. It is therefore important to carefully consider all available tax options before making a decision.

Investor status as an individual reviewed

The second change concerns the status of individual investor. Previously, individuals could be considered professionals if they reached a certain threshold of capital gains or transactions. That meant they were subject to the industrial and commercial benefits regime (BIC), with a tax rate up to 66.2%.

The Ministry of Economy, Finance, Industrial and Digital Sovereignty decided to modify this qualification to include any transfer of cryptoassets carried out “in a non-professional capacity”, in the framework for managing one's own private assets. This new qualification leads to the application of the flat tax regime, regardless of the amount or volume of transactions carried out.

The case of professionals' earnings clarified

Traders now have a tax liability as non-commercial profits (BNC). Previously, they were subject to the Industrial and Commercial Benefits (BIC) regime, but from now on, they will be “subject to the Tax and social security contributions schedule, after deduction of a 34% reduction (micro-BNC regime) or expenses related to the activity (controlled declaration regime).” This change results in a more favorable method of calculating profits for professionals.

The latter were put at a disadvantage by the old method, which consisted of taxation in real time rather than when earnings were withdrawn. This forced some professionals to sell assets, even when prices were not favorable, in order to pay their taxes. It is important to note that there is no no change for capital gains made on cryptocurrency mining, which remain affiliated to the BNC regime.

Cryptocurrency taxation: do you have to pay taxes?

Cryptocurrencies have long escaped the radar of the French tax administration, creating legal uncertainty that is harmful to investors. This period ended on January 1, 2019. The articles 150 HP and 200 C of the General Tax Code as well as the BOFIP BOI-RPPM-PVBMC-30 Imposing the calculation and declaration of capital gains realized on digital assets. This declaration must be made at the same time as the traditional income tax return. The absence of a declaration will be punishable by a fine and may result in a tax adjustment.

The sale of a cryptocurrency to fiat currencies (such as the euro or the dollar) therefore triggers a tax reporting obligation. Also concerned are Sales with soulte, or sales in which you receive one part in crypto and the other in fiat (euro). Good news, transactions Crypto-crypto (ex: selling BTC against ETH) are not taxed because they are considered to be “unpaid”. Elles therefore evade taxation and the obligation to report. As long as you stay in crypto, your wealth management Don't does not require tax declarations on capital gains.

Finally, the purchase of consumer goods in cryptocurrency also triggers A tax obligation. If you plan to buy your Tesla in BTC, you will have to remember to declare the purchase and pay the tax generated by the bitcoin tax!

Good to know : If the crypto/fiat sales made over a fiscal year are less than €305, they are exempt from crypto taxes. It is the only true measure of tax exemption cryptocurrencies currently in force.

Trading frequency determines your cryptocurrency tax

The rate applied on capital gains is that of flat tax (or single flat rate), i.e. 30%. You will therefore pay the same taxes for capital gains in shares (held on a securities account) than those carried out on cryptos. This rate is broken down as follows: 12.8% taxes and 17.2% CSG-CRDS.

In order to take advantage of this rate, the crypto trading activity must be carried out on an occasional basis. If the activity is carried out on a regular basis, the rate will be higher since it will be subject to BNC (non-commercial benefits), either income tax + CSG-CRDS. According to the tax authorities, the difference between the casual and the usual is based on the time between the purchase and the resale of the asset. In other words, if you are trading Intraday, there is a good chance that the administration will consider this activity to be routine. One”Hodlers“Who manages the wealth of a father of a family falls into the “casual activity” box and will have a relaxed cryptocurrency taxation.

Here is what the tax authorities specify:

The criteria for the usual or occasional exercise of the activity result from the examination, on a case-by-case basis, of the factual circumstances in which the purchase and resale operations are carried out (the time between the dates of purchase and resale, the number of bitcoins sold, the conditions of their acquisition, etc.)

There is therefore no official threshold separating usual and professional, which leaves room for doubt... The analysis will be done on a case-by-case basis., and other criteria such as the trader's know-how and sophistication (use of bots, derivatives strategies or hedging) can also play a role. In addition, the administration will have a definite interest to requalify an individual as a professional in order to increase the tax bill.

Track your crypto performance!

https://www.youtube.com/watch?v=P-SzFssdAnA&ab_channel=Finary

Declaring cryptocurrency: what is not concerned

If you own one or more of the cryptos listed below, you will be happy to know that they do not generate any related tax obligations.

NFT crypto: The”Non Fungible Tokens” are unique tokens, unlike ETH or BTC where no token is the same as another. They are very popular for NFT art and major artists like Justin Roiland, creator of Rick and Morty, have made sales in this format. They are assimilated to physical goods by the tax authorities.

Stablecoins: The stablecoin is a token backed by a currency. For example, USDC is worth $1. A BTC-USDC transaction is therefore out of scope for the tax on digital assets.

Security Tokens: these tokens are digital equivalents of a physical asset, for example a building. They are also out of scope for taxation.

Defi Crypto: there is currently a lack of clarity on the fiscal obligations associated with DeFi. What about farming, pooling and others Staking ? The future will tell us!

Calculate your cryptocurrency taxation

Now that we have set the framework, let's focus on calculating this added value. This calculation must be carried out on all crypto sales made during the reference period, for example the fiscal year 2020. If you don't like math, you're in for a treat...

Case of selling all of your cryptos

Let's start with the simplest scenario, which is selling all of your digital assets.

- February 2022 : Deposit of 5000€ on an exchange

- February 2023 : Purchase of 1 BTC for €5,000

- February 2023 : Sale of 1 BTC for €10,000

Selling BTC for added value triggers bitcoin taxation. Here is the calculation:

- Added value : 10,000 - 5,000 = 5,000€

- taxation : €5,000 * 30% = €1500

The capital gain amounts to €5,000 and the taxpayer will have to pay €1500 in taxes for the 2020 fiscal year.

If he owned several cryptos (e.g. ETH, BTC and LTC), it would have been necessary to sum up the sales in order to know the added value. Indeed, it is the overall added value that is taken into account

Partial sale of your cryptocurrencies

This relatively simple scenario does not take into account the possibility that the investor has purchased several different cryptos. Now let's look at this case:

- February 2022 : deposit (or cash-in) of €10,000 on an exchange

- February 2022 : purchase of 1 BTC for 5000€ and 50 ETH for 100€

- February 2023: The price of cryptos has increased sharply, 1 BTC is now worth €10,000, while one ETH is worth €250

- February 2023 : Sale of 0.5 BTC for €5,000 and 25 ETH for €6,250, or €11,250

Good to know: whether the money stays on the platform or if they come back into your accounts, the tax treatment is the same: you have to declare the capital gain and pay the flat tax on it.

The person sold 50% of his BTC and 50% of his ETH for fiat (€), cryptocurrency taxation applies. It is necessary to calculate the ratio between cash in (deposit) and cash out (sales) to find out the final amount to be paid.

Here are the calculation steps:

Overall value of the portfolio at the time of sale:

- In crypto: 1 BTC (€10,000 per BTC) and 50 ETH (€250 per ETH)

- In fact: €10,000 + €12,500 = €22,500

The stages of the sale in a fiscal sense:

- Overall value of the sale made (cash-out): 0.5 * 10,000 + 25 * 250 = 11,250€

- Share of portfolio sold (% cash-out): 1250/2,500 = 50%

- Plus taxable value (formula): cash-out - cash-in * (% cash-out)

- Taxable capital gain: €11,250 - €10,000 * 50% = €6,250

- Flat rate: €6,250 * 30% = €1,875

- Remaining cash out: €3,750

The taxpayer must therefore pay €1,875 tax on his crypto earnings in 2020. He will be left €3,750 cash out to be deducted from future sales.

Note that you may therefore find yourself having to pay taxes in excess of the capital gain in the event that the overall crypto wallet is very important. Indeed, the method of calculation in force takes into account the unrealized capital gains of this same global portfolio. We can even theoretically sell crypto at a loss and be liable for crypto taxes. Funny era.

How do I declare cryptocurrency taxation?

Once the capital gains have been calculated, you have to start the heavy task of declaring these gains. Again, this is anything but trivial and you will have to fill out several forms, including the Deer 2042.

Electronic declaration and crypto taxation

If you file your crypto taxes online, you will be delighted to learn that the procedure is greatly simplified. Here are the steps to find the right forms.

- Revenues: check the box “Gains from the sale of securities...”

2. Selection of Appendices

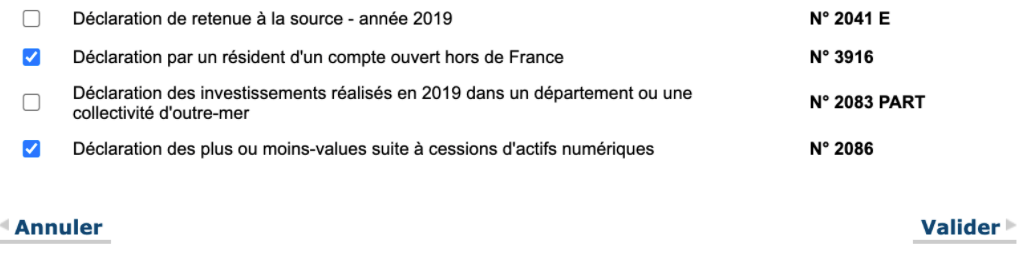

3. Selecting the Form 3916 And of Cerfa 2086

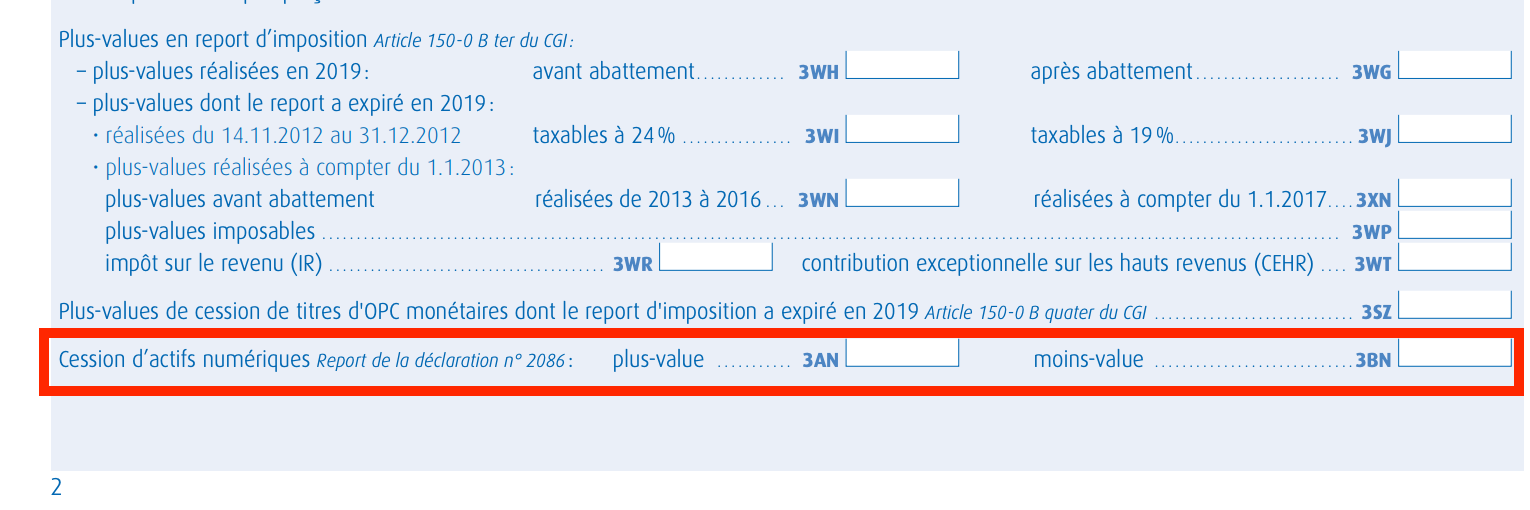

4. Once 2086 is filled in, boxes 3AN and 3BN of Form 2042 will also be updated.

Let's go back in detail to each of these forms in order to fully understand what they are for and how to fill them out.

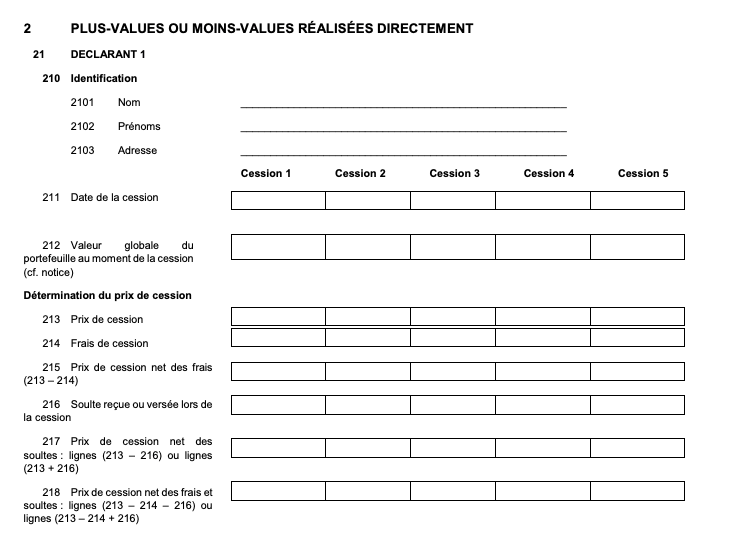

Declaration of realized capital gains (Cerfa 2042)

Once the capital gain has been calculated, it must be declared in the corresponding form. In our case, it is the Cerfa 2042 C dedicated to additional tax returns. Remember that the 2020 capital gains declaration will be made in 2021.

Here are the boxes to fill out:

- 3 YEARS: In case of capital gain: in our example mentioned above, 6250€ should be indicated

- 3BN: To be completed in case of loss of value

Declaration of digital asset sales (Cerfa 2086)

This form is a small novelty in the world of tax forms which is exclusively dedicated to cryptos. You will find the calculations indicated above as well as the concept of balance.

As indicated above, Annex 2086 is available directly online in the appendix section of your tax return.

Foreign account statement for cryptocurrency taxation

Exchanges are not particularly useful in guiding you through the thorny subject of cryptocurrency taxation. To date, none offers a service dedicated to calculating taxes. On the other hand, having an account on an exchange platform will trigger additional tax liabilitye, the foreign account statement.

If you have an account with a French platform like Coinhouse or Paymium, you don't have to declare anything. These platforms automatically transmit your information to the tax authorities.

Good to know: Cold wallets (like Ledger or Trezor) are not affected by cryptocurrency taxation, so you don't have to declare anything as long as you do HODL on them.

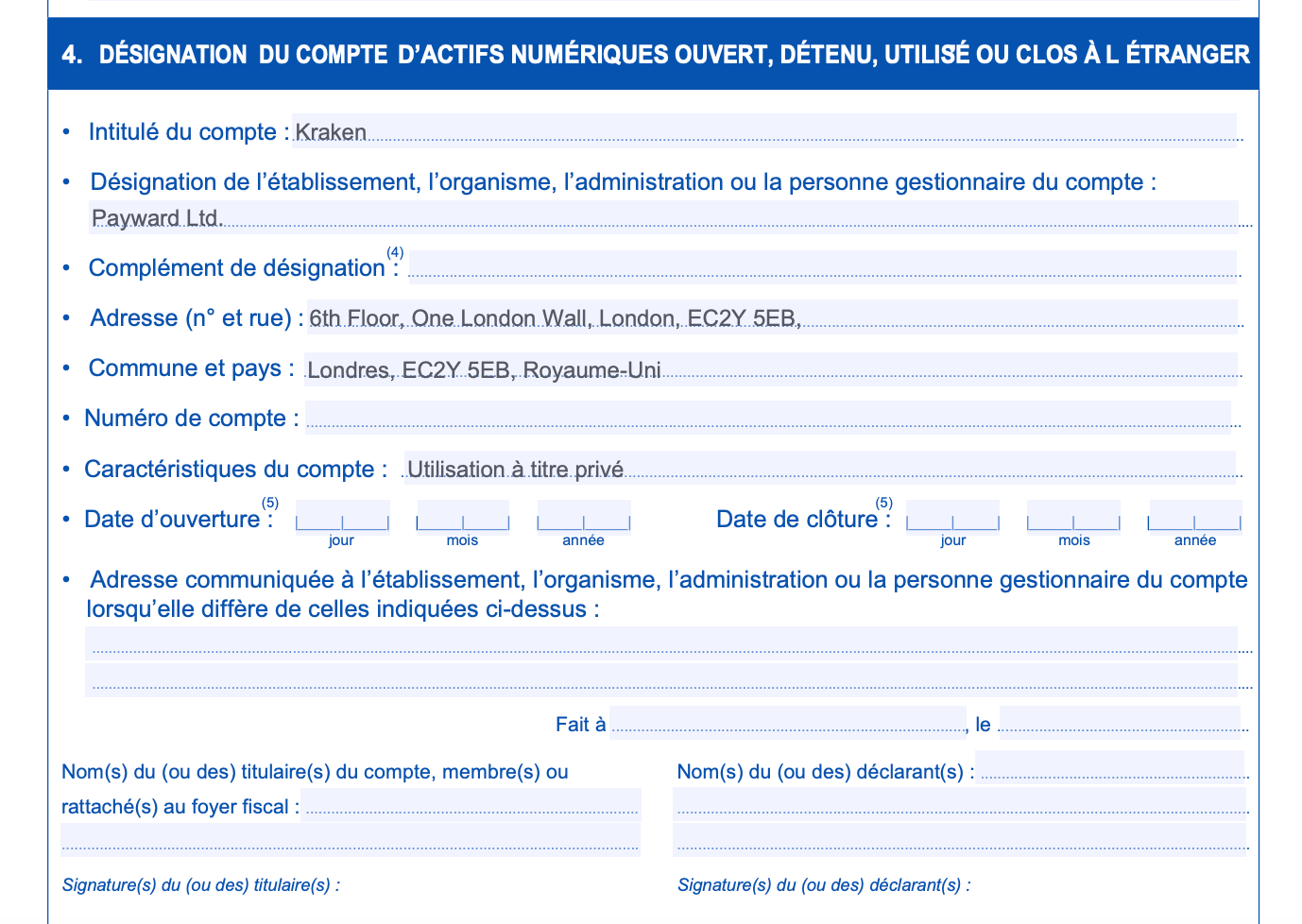

Complete Form 3916 without making mistakes

Since the majority of trading platforms are located abroad, they are counted as foreign accounts. This time it's the Cerfa 3916 that will have to be filled out. Binance, Kraken, Bitstamp or Crypto.com, you will have to fill out a form for each of them. Declaring a Coinbase account is not a choice, it is an obligation.

This form has a number of fields that we will review:

- Account title: free title, for example the name of the exchange.

- Designation of the establishment: legal name of the exchange, for example Payward Ltd for Kraken.

- Adress: Head office of the company. It may vary depending on which bank you made deposits to.

- Account number: available in your account on some exchanges. If you can't find it, your email will suffice.

- Account characteristics: Indicate the type of account, for example “joint account” or “private account”.

Good to know: Holders of a Revolut or N26 account already know the Cerfa 3916. Indeed, as these banks are also located abroad, they must be declared in the same way as crypto platforms.

Cryptocurrency fraud and taxation

Who says taxation says tax adjustment. Crypto is no exception to the rule and fines for breaches can be very heavy. Forgetting to declare a Coinbase account can result in a fine of €750, and this per undeclared account. If the value of the cryptos held on the account is greater than €50,000, it may even reach €1,500.

If the country has not signed an administrative agreement with France, the fine can even reach €10,000. These fines may seem very high given the complexity of the declarations to be made... Good news: Accounts closed before 2019 are not to be reported, no cryptocurrency tax for them.

In the event of a tax adjustment, the fine may be increased up to 80% of the initial amount, which makes fraud extremely expensive and anything but encouraged. If the tax authorities send you an inspection notice, you can contest it. This will open up a litigation phase that may be costly in terms of legal fees and still lead to tax recovery. In short, trying to evade cryptocurrency taxation can be expensive.

Follow her Cryptocurrency performance with Finary!

What about cryptocurrency taxation abroad?

Cryptocurrency taxes vary enormously from one country to another and several countries in the European Union have adopted radically opposed positions to that of France.

Is Germany a tax haven?

Germany decided to consider cryptos as means of payment. After 1 year of holding a crypto asset, capital gains do not generate any cryptocurrency taxes. This choice is quite deliberate: Germany wants to attract crypto talent and companies because it knows that this technology will create a lot of wealth in the years to come. A sign that it's working: the IOTA foundation has moved to Berlin. Instead of punishing crypto holders, it encourages them !

Note that this bitcoin tax exemption only applies to individuals, professionals are treated differently.

What about cryptocurrency taxation in Belgium?

Belgium followed Germany in terms of taxes: crypto capital gains are simply tax exempt for an investor who makes HODL. Portugal has adopted the same position, making it another top destination for crypto millionaires. Our Swiss neighbours have also made this choice: Swiss cryptocurrency taxation on capital gains amounts to 0%, making the country particularly attractive. Moreover, the Ethereum foundation understood this well by establishing its headquarters in the canton of Zug.

Frequently asked questions about cryptocurrency taxation

Do you have to pay taxes on cryptocurrencies? If you sold cryptocurrencies like Bitcoin or Ethereum for euros and made a profit, yes. The declaration must be made the year following the sale (N+1). The applicable rate will be that of the flat tax, i.e. 30%. If you have made losses, you will have to report them but you will not have to pay anything. If you sold cryptocurrencies for other cryptocurrencies, you are not taxable.

Do you have to declare your cryptocurrency accounts? Yes! Since 2019, you have been required to declare all accounts (Coinbase, Kraken, Binance etc.) on which you hold cryptos (or digital assets) via the Cerfa 3916 form.

What is the cryptocurrency tax rate? For the vast majority of investors, it will be the flat tax of 30% that will apply to capital gains. This rate, also called single lump-sum levy (PFU), applies only to the capital gain, i.e. the difference between the purchase price and the sale price.

How not to pay crypto tax? Since cryptos-crypto transactions are not taxed, you will not pay taxes until you switch back to Euros or Dollars. You can also sell your cryptos against stablecoins like USDT or USDC in order to secure a profit without triggering tax obligations.

How to avoid crypto flat tax? If, for example, on this tax regime you exchange Bitcoin for Ethereum (ETH) or any other cryptocurrency, this operation is exempt from tax, even if you have realized a gain in value. This exemption also applies to exchanges made on cryptocurrency trading platforms.

This article and all information contained in it is provided for informational purposes only and does not constitute tax or investment advice.